Direct Lending vs. Broker-Led Vehicle Finance in Australia: A Complete Guide

Navigating the landscape of Vehicle Finance in Australia has become increasingly complex as we move through 2026. With fluctuating cash rates and a diverse array of lending products, car buyers are often torn between going directly to a bank or utilizing a specialized finance broker. Understanding the mechanics of each pathway is essential to securing a deal that aligns with your long-term financial health. Whether you are purchasing a family SUV or a fleet for your business, the method you choose to secure your funding will significantly impact your total cost of ownership.

Securing the right asset finance is just one piece of your broader financial puzzle. If you are looking to optimize your entire portfolio, you might also consider consulting a Refinance Home Loan Broker to ensure your mortgage and vehicle repayments are working in harmony. Expert guidance across all forms of credit can lead to substantial savings over time, allowing you to allocate capital toward other life goals or business expansions.

Understanding Direct Lending for Vehicle Finance in Australia

What is Direct Lending?

Direct lending occurs when a borrower applies for a loan directly through a financial institution, such as a major bank or a credit union. In the context of Vehicle Finance in Australia, this is often the “traditional” route where a customer uses their existing banking relationship to secure a car loan.

The Convenience of Existing Relationships

Many Australians prefer direct lending because of the “one-stop-shop” feel. If you already have a savings account or mortgage with a bank, the application process for Vehicle Finance in Australia can sometimes be streamlined since the bank already has your financial history on file.

Transparency in Rates

When you deal directly with a lender, the rates are usually non-negotiable and publicly listed. While this lacks flexibility, it provides a level of certainty for those who prefer not to haggle. You can easily see the Best Car Loan Rates Australia-wide on a bank’s website and decide if they meet your criteria.

The Rise of Broker-Led Vehicle Finance in Australia

How Finance Brokers Operate

A finance broker acts as an intermediary between you and a panel of dozens of different lenders. For Vehicle Finance in Australia, a broker doesn’t just look at one bank’s products; they compare options from “Big Four” banks, non-bank lenders, and boutique credit providers to find a match for your specific credit profile.

Access to Wholesale Rates

Brokers often have access to “wholesale” rates that are not advertised to the general public. This is a primary reason why many find that a broker can beat the Best Car Loan Rates Australia offered by retail banks. They leverage their high volume of business to negotiate better terms for their clients.

Expertise in Specialized Loans

If you are looking for Low Interest Used Car Loans, brokers are particularly effective. Traditional banks can be rigid regarding the age of the vehicle, whereas brokers can find specialized lenders who offer competitive terms for older models or unique vehicle types.

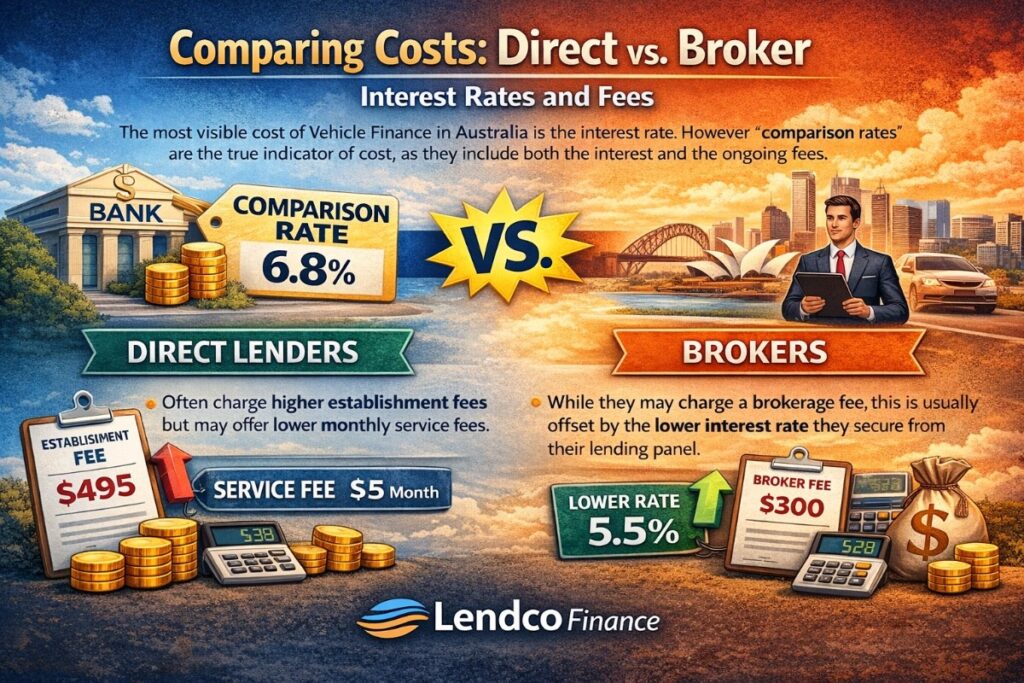

Comparing Costs: Direct vs. Broker

Interest Rates and Fees

The most visible cost of Vehicle Finance in Australia is the interest rate. However, “comparison rates” are the true indicator of cost, as they include both the interest and the ongoing fees.

- Direct Lenders: Often charge higher establishment fees but may offer lower monthly service fees.

- Brokers: While they may charge a brokerage fee, this is usually offset by the lower interest rate they secure from their lending panel.

2026 Market Analysis Table

To visualize the potential difference in Vehicle Finance in Australia, consider this hypothetical comparison based on a $40,000 loan over 5 years:

| Feature | Direct Bank Loan | Broker-Led Loan |

| Average Interest Rate | 7.50% p.a. | 6.45% p.a. |

| Establishment Fee | $250 | $0 – $395 |

| Monthly Fees | $10 | $0 |

| Total Interest Paid | $8,140 | $6,920 |

| Total Savings | **$0** | $1,220+ |

Impact on Credit Scores

Every time you apply directly to a bank, a “hard inquiry” is recorded on your credit file. If you apply to three different banks to compare Vehicle Finance in Australia, your score may drop. A broker, conversely, performs a “soft search” or a single credit pull to shop your profile around, protecting your credit standing while finding Low Interest Used Car Loans.

Business and Commercial Considerations

Commercial Vehicle Finance for Tradies and SMEs

For business owners, Vehicle Finance in Australia is not just about the monthly payment; it is about tax effectiveness. Commercial Vehicle Finance structures like Chattel Mortgages or Novated Leases offer different GST and depreciation benefits.

- Chattel Mortgage: You own the vehicle from day one, and the lender takes a “mortgage” over it as security.

- Novated Lease: A three-way agreement between you, your employer, and the lender that allows for “salary packaging” your car.

Flexibility in Repayment Structures

Brokers often excel in Commercial Vehicle Finance by arranging seasonal repayments or “balloon” payments. This is crucial for Queensland businesses that may experience cyclical cash flows and need their Vehicle Finance in Australia to be as flexible as their operations. You can learn more about Australian lending standards via the ASIC MoneySmart website.

Navigating the Used Car Market

Challenges with Pre-Owned Vehicles

Securing Low Interest Used Car Loans directly from a bank can be difficult if the car is more than 5–7 years old. Direct lenders view older assets as higher risk and often increase interest rates accordingly.

Why Brokers Win on Used Cars

Brokers work with “asset-based” lenders who specialize in older vehicles. By understanding the valuation of the car, they can secure Vehicle Finance in Australia that doesn’t penalize you for buying a reliable second-hand workhorse instead of a brand-new luxury vehicle.

Verification and Safety

A good broker doesn’t just find the money; they often help verify that the used vehicle has a clear title (PPSR check). This added layer of security makes the process of obtaining Vehicle Finance in Australia much safer for the consumer.

Trends in Australian Vehicle Finance for 2026

The Shift Toward Green Finance

With Australia’s push toward electric vehicles (EVs), many lenders are offering “Green Loans.” These are effectively Low Interest Used Car Loans (or new car loans) specifically for low-emission vehicles.

Digital-First Applications

The “Direct vs. Broker” debate is now happening entirely online. Whether you choose a direct neobank or a digital brokerage, the speed of Vehicle Finance in Australia has increased, with some approvals happening in minutes rather than days.

Strategic Steps to Prepare for a Vehicle Finance Application

Assessing Your Credit Readiness

Before applying for Vehicle Finance in Australia, it is vital to understand your credit standing. Lenders and brokers alike will evaluate your “character” based on your repayment history and existing debt-to-income ratio. In 2026, many Australians will use free credit-checking tools to identify any discrepancies before they sit down with a professional. A higher credit score not only unlocks the Best Car Loan Rates Australia has to offer but also provides more leverage when negotiating loan terms or balloon payments.

Gathering the Necessary Documentation

To ensure a smooth approval process, you should have your financial documents organized in advance. Typically, for Vehicle Finance in Australia, you will need:

- Proof of Identity Income Verification: Your most recent two pay slips or, for business owners, the last two years of tax returns.

- y: A valid Australian Driver’s License or Passport.

- Bank Statements: Usually the last 90 days of transactions to demonstrate your spending habits and ability to service the loan.

- Asset and Liability Statement: A simple list of what you own versus what you owe.

Long-Term Financial Impact: Beyond the Monthly Payment

Total Cost of Ownership Analysis

When people think about Vehicle Finance in Australia, they often focus solely on the “monthly repayment” figure. However, a truly savvy borrower looks at the total cost of ownership (TCO). This includes the total interest paid over the life of the loan, any hidden “exit fees” for early repayment, and how the finance structure affects the vehicle’s resale value. For instance, while Low Interest Used Car Loans might have slightly higher rates than new car loans, the lower initial depreciation on a used vehicle often leads to a better TCO.

Flexibility and Refinancing Options

Life circumstances can change rapidly. The most robust Vehicle Finance in Australia plans include the flexibility to make extra repayments without penalty or the option to refinance if interest rates drop significantly in the future. Working with a broker is often advantageous here, as they can identify which lenders are “refinance-friendly.” This ensures that your vehicle debt remains an asset to your lifestyle or business, rather than a rigid financial burden that limits your future borrowing power for other milestones.

Conclusion

Choosing between direct lending and a broker-led approach for Vehicle Finance in Australia ultimately depends on your financial complexity and the time you have available. Direct lending offers the comfort of familiarity, but it often lacks the competitive edge found in the broader market. In 2026, the data suggests that utilizing a broker provides a significant advantage by accessing wholesale rates, protecting your credit score, and offering tailored solutions for Commercial Vehicle Finance and specialized used car lending.

If you are ready to see how much you could save on your next purchase, our team is here to help you navigate the best Vehicle Finance in Australia. We take the guesswork out of the process, comparing dozens of lenders to ensure you get the most competitive deal possible. Contact us today to get a quote and take the first step toward your new vehicle with confidence.

Frequently Asked Questions

Does using a broker for vehicle finance in Australia cost more?

Generally, no. While brokers may charge an upfront fee, they typically secure a lower interest rate than you could get on your own. This results in a lower total cost over the life of the loan.

Can I get low interest used car loans for a car over 10 years old?

Yes, but it is much easier through a broker. Traditional banks often have a cut-off age for vehicles, but specialized lenders on a broker’s panel are more flexible with older assets.

What is the difference between a car loan and commercial vehicle finance?

A car loan is for personal use, while commercial finance is designed for business-use vehicles. Commercial options often provide tax benefits like GST input tax credits and depreciation.

Will shopping around for the best car loan rates Australia-wide hurt my credit?

If you apply directly to multiple banks, yes. Each application is a “hard hit.” Using a broker allows you to compare multiple lenders with only one initial credit inquiry, protecting your score.

How long does approval for vehicle finance in Australia take in 2026?

Thanks to automated credit decisioning, many lenders now provide “conditional approval” within minutes. Final settlement typically takes between 24 and 48 hours once all documents are signed.

Is it better to have a balloon payment on my vehicle finance?

A balloon payment lowers your monthly costs by deferring a large chunk of the principal to the end of the loan. It’s great for cash flow but means you will pay more in total interest.