Complete Guide to Choosing a Motorbike Finance Broker in Gold Coast

Finding the freedom of the open road on a new motorcycle is a dream for many residents in Queensland, but navigating the financial path to get there can be complex. Choosing a professional Motorbike Finance Broker is the most effective way to secure a deal that fits your budget without the stress of dealing directly with rigid bank structures. A local broker understands the Gold Coast market, offering personalized service that ensures you aren’t just another number in a giant corporate database.

When you work with experts who understand the local lending landscape, you gain access to a wider variety of loan products. For those who are also looking into property, finding the Best Mortgage Brokers in Australia can provide a holistic view of your financial health. This guide will deep dive into how a specialized broker can transform your buying experience from a headache into a high-speed success.

Why Use a Motorbike Finance Broker in Gold Coast?

The Gold Coast lifestyle is synonymous with outdoor adventure, making motorbikes a popular choice for both commuting and weekend coastal runs. However, many buyers make the mistake of taking the first offer from a dealership.

Expertise in Specialized Lending

A Motorbike Finance Broker specializes in leisure assets. Unlike standard car loans, motorbike loans can sometimes have different risk profiles or residual value calculations. A broker knows which lenders are “bike-friendly” and which ones offer the lowest interest rates for specific types of motorcycles, whether it’s a cruiser, a sports bike, or an off-road adventurer.

Saving Time and Effort

Instead of spending hours comparing websites and filling out multiple applications—which can actually damage your credit score—a broker does the heavy lifting. They act as the intermediary between you and dozens of potential lenders, streamlining the process so you can focus on picking out your gear.

Understanding the Different Types of Motorbike Loans

Before settling on a Motorbike Finance Broker, it is essential to understand the products they might offer. Each loan type has its own set of advantages depending on your employment status and how you plan to use the bike.

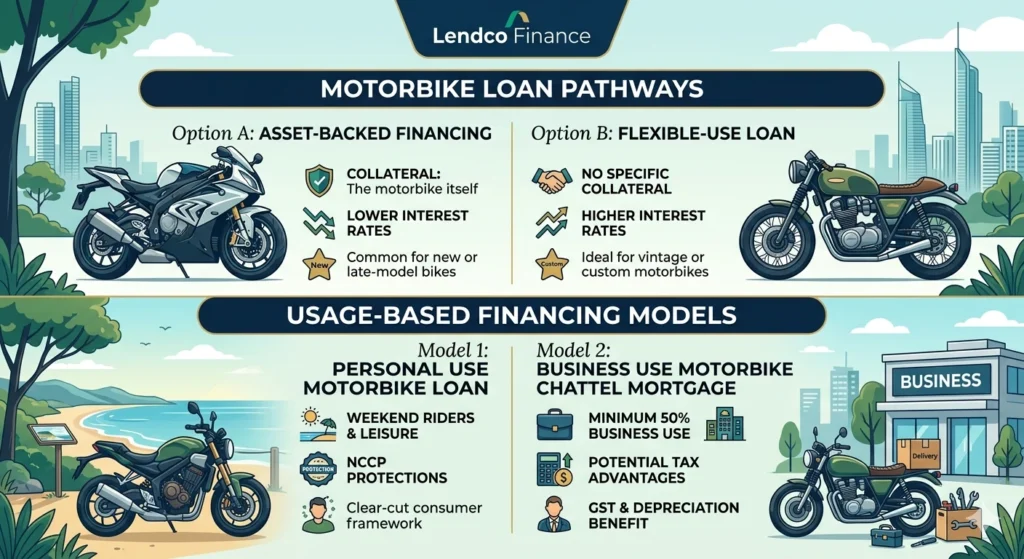

Secured vs. Unsecured Loans

Secured Motorbike Loans

In a secured loan, the motorcycle itself acts as collateral. Because the lender has a safety net, these loans typically come with lower interest rates. This is the most common path for new or near-new bikes.

Unsecured Motorbike Loans

If you are buying an older vintage bike or a custom build that doesn’t meet standard collateral criteria, your Motorbike Finance Broker might suggest an unsecured loan. While the rates are slightly higher, you have more flexibility with what you buy.

Consumer vs. Commercial Finance

Personal Use Loans

If the bike is strictly for weekend rides through the Hinterland, a standard consumer loan is the way to go. These are regulated by the National Consumer Credit Protection (NCCP) Act, providing you with specific legal protections.

Chattel Mortgages for Business

If you use your motorbike for business purposes at least 50% of the time, a Chattel Mortgage can offer significant tax benefits. Your Motorbike Finance Broker can explain how GST input tax credits and depreciation might apply to your purchase.

How to Evaluate a Motorbike Finance Broker

Not all brokers are created equal. When searching for a Motorbike Finance Broker on the Gold Coast, you need to look for specific markers of quality and transparency.

Licensing and Compliance

Every reputable broker in Australia must hold an Australian Credit License (ACL) or be an authorized representative of a licensee. This ensures they adhere to “Best Interests Duty,” meaning they are legally obligated to act in your best financial interest, not the lender’s.

Panel of Lenders

The strength of a Motorbike Finance Broker lies in their “panel.” A broker with only three or four lenders is essentially a glorified salesperson for those brands. Look for brokers who have access to 30+ lenders, including:

- Big Four Banks

- Boutique Credit Unions

- Non-bank specialized lenders

- Peer-to-peer lending platforms

Transparency in Fees

A good broker will be upfront about how they are paid. Usually, they receive a commission from the lender, but some may charge an additional brokerage fee. Ensure these are disclosed in the Credit Quote or Credit Proposal before you sign anything.

The Benefits of Local Gold Coast Expertise

While online-only brokers exist, there is a distinct advantage to using a local Motorbike Finance Broker.

Knowledge of Local Dealerships

Local brokers often have established relationships with dealerships across Nerang, Burleigh Heads, and Southport. They can sometimes coordinate the finance and delivery more smoothly because they know the staff and the processes of local businesses.

Face-to-Face Consultations

In an increasingly digital world, being able to sit down with your Motorbike Finance Broker provides a level of comfort and clarity that an automated chat-bot cannot match. They can explain complex terms like “balloon payments” or “comparison rates” in plain English.

The Loan Application Process: Step-by-Step

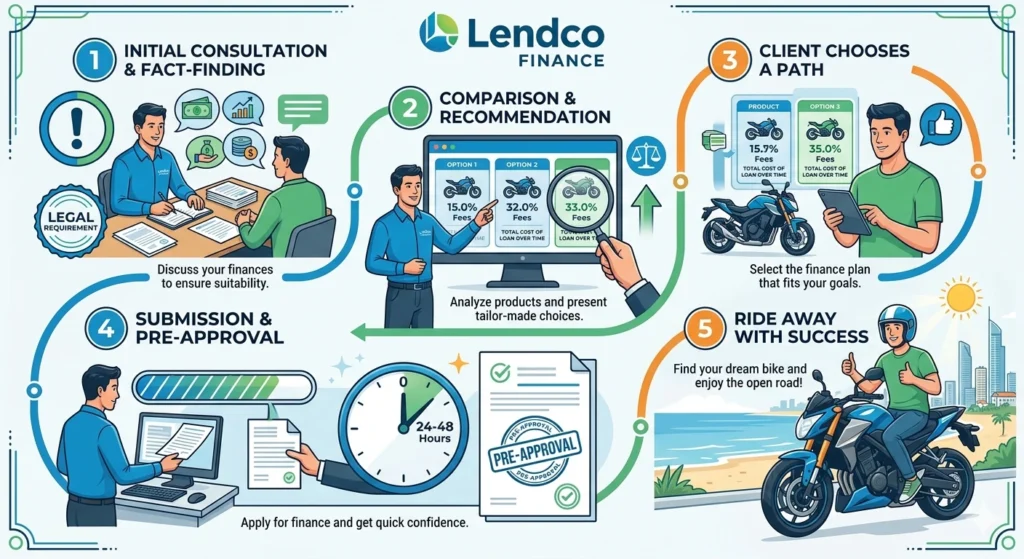

Understanding the timeline helps manage expectations. A professional Motorbike Finance Broker will typically follow this trajectory:

Initial Consultation and Fact-Finding

The broker will ask about your income, expenses, assets, and liabilities. This isn’t just “prying”—it’s a legal requirement to ensure the loan is “not unsuitable” for you.

Comparison and Recommendation

The Motorbike Finance Broker will compare various products and present you with a few options that meet your specific needs, highlighting the total cost of the loan over time.

Submission and Approval

Once you choose a path, the broker submits the formal application. On the Gold Coast, many brokers can get “Pre-Approval” within 24 to 48 hours, giving you the confidence to negotiate with sellers.

Comparing Broker Services: What to Look For

| Feature | Local Broker | Online “Quick” Broker | Direct Bank |

| Lender Choice | High (30+ Lenders) | High (Varies) | Low (1 Lender) |

| Personalized Advice | Excellent | Minimal/Automated | Limited to own products |

| Speed of Approval | Fast (Direct Contact) | Very Fast | Slow to Moderate |

| Niche Bike Knowledge | High | Low | Very Low |

Common Pitfalls to Avoid in Motorbike Finance

Even with a Motorbike Finance Broker, you should stay vigilant. Many buyers fall into traps that end up costing thousands over the life of the loan.

Focusing Only on Monthly Payments

A low monthly payment might look attractive, but if it’s stretched over seven years with a massive balloon payment at the end, you will pay significantly more in interest. Always ask your Motorbike Finance Broker for the “Total Cost of Credit.”

Overlooking the Comparison Rate

The “headline” interest rate is often lower than the “comparison” rate. The comparison rate includes most fees and charges, giving you a truer picture of the loan’s cost. For more information on how financial regulations protect you in Australia, you can check the Moneysmart website for official guidelines.

Not Checking for Early Exit Fees

If you plan to pay your bike off early, ensure your Motorbike Finance Broker finds a loan that doesn’t penalize you for being financially responsible. Some lenders charge hefty fees if you close the account before the term ends.

Credit Scores and Your Finance Broker

Your credit score is the single most important factor in determining your interest rate. A Motorbike Finance Broker plays a crucial role here.

Protecting Your Credit File

Every time you apply for a loan and get rejected, it leaves a “hard inquiry” on your file. A Motorbike Finance Broker will assess your profile first and only apply to the lender most likely to approve you, protecting your score from unnecessary dings.

Helping with “Bad Credit”

If you have a few marks on your credit history, don’t despair. Specialized brokers have access to “second-tier” lenders who look at your current ability to pay rather than just your past mistakes.

Future Financial Planning

A motorbike is an exciting purchase, but it is often just one part of your broader financial journey. If you are currently managing multiple properties or looking to expand your portfolio, consulting an Investment Mortgage Broker can help ensure your motorbike loan doesn’t negatively impact your borrowing power for future investments.

Conclusion

Securing the right deal requires more than just looking at the price tag of the bike; it requires a strategic approach to lending. By partnering with a dedicated Motorbike Finance Broker, you gain an advocate who understands the nuances of the Gold Coast market and the specifics of motorcycle lending. They provide the bridge between your dream of riding and the reality of a sustainable, affordable loan. Take the time to research, check reviews, and choose a broker who prioritizes transparency and communication.

Ready to hit the road? Our team is here to help you navigate every turn of the financing process. Contact us today to speak with an expert and see how easy getting a motorbike loan can be.

Frequently Asked Questions

What does a Motorbike Finance Broker actually do?

A broker acts as an intermediary between you and potential lenders. They assess your financial situation, find the most competitive loan products from their panel, and handle all the paperwork and negotiations to secure your approval.

Is it more expensive to use a Motorbike Finance Broker?

Generally, no. Brokers are typically paid a commission by the lender. While some may charge a separate brokerage fee for complex cases, the interest rates they access are often lower than what you could get as an individual walking into a bank.

Can I get a loan for a used bike through a broker?

Yes, a Motorbike Finance Broker can secure financing for both new and used motorcycles. For used bikes, lenders may have specific age restrictions, but a broker will know exactly which lender to approach based on the bike’s year and condition.

How long does the approval process take?

In many cases, a broker can get you a pre-approval within 24 to 48 hours. Once you have chosen a specific bike and provided the necessary documents, final settlement usually occurs within 3 to 5 business days.

Do I need a deposit for a motorbike loan?

Not necessarily. While having a deposit can lower your monthly payments and improve your chances of approval, many brokers can facilitate 100% financing (no deposit) for applicants with strong credit profiles.

Will a motorbike loan affect my ability to get a mortgage?

Yes, any debt you take on will be considered a liability and can affect your “serviceability” for a home loan. This is why it is important to speak with your Motorbike Finance Broker about your long-term goals before signing.