Life doesn’t usually wait for your savings to catch up. Bills pile up, and business ideas often need a green light long before you’ve hit your savings goal. That’s where Unsecured Finance comes in; there’s no mountain of paperwork and no need to put your house on the line. It’s just about getting the funds when the timing is right.

All over Australia, we’re seeing more young pros and business owners turning to unsecured loans as a common-sense option. It’s the speed and lack of strings that really appeal. Thanks to providers like Lendco Finance, obtaining a loan no longer has to be a daunting task.

Real-world borrowing rarely fits into neat boxes. A loan taken to smooth a rough month can quietly turn into a long-term commitment if not handled properly, so finding all your loan solutions requires a clear strategy. Understanding the mechanics, rather than just the marketing, is crucial.

Understanding unsecured finance in modern Australia

The idea behind Unsecured Finance is simple enough: borrow without putting up assets. But in practice, it’s layered. Lenders rely heavily on credit behaviour, income consistency, and spending patterns. It’s less about what is owned and more about how financial responsibility is demonstrated over time.

In the Australian lending landscape, this approach has grown steadily. Not explosively, but consistently. Many borrowers aren’t interested in tying their home or vehicle to a loan anymore. There’s a growing awareness of risk, especially after seeing how quickly financial situations can shift. That caution has made unsecured lending more appealing, even if the cost is slightly higher.

There’s also a behavioural angle. Borrowers using unsecured options tend to be more conscious of repayment structures. Without an asset at risk, discipline becomes the key safeguard. Interestingly, lenders have adapted too, using smarter data systems to assess risk more accurately rather than relying purely on collateral.

Why borrowers choose speed over loan security today

Speed has quietly become one of the most valuable features in lending. Not advertised loudly, but deeply felt. Waiting ten days for approval might have been acceptable a decade ago. Now, it feels excessive.

In real scenarios, delays cost money. A small business missing out on inventory discounts or a professional unable to cover an urgent expense—these aren’t hypothetical situations. They happen often. Unsecured Finance reduces that lag significantly, and that’s where its real value shows up.

That said, speed isn’t always a perfect advantage. Quick approvals can sometimes encourage rushed decisions. There’s a tendency to overlook repayment structures or underestimate long-term costs. Seasoned borrowers usually pause even briefly before committing. That small pause often prevents a larger financial strain later.

How Lendco Finance simplifies unsecured borrowing fast

Lendco Finance seems to get that people are busy. Their whole approach to Unsecured Finance feels like it was built for real life. You don’t have to spend hours decoding jargon or hunting down documents across five different platforms just to get an answer.

The applications move fast, but they aren’t sloppy. The checks and approvals are streamlined, ensuring that understanding personal loans and credit in Australia remains a priority for keeping things responsible. Finding the middle ground between too slow and too simple is harder than it looks, but that’s what sets a good lender apart.

From a user perspective, the experience tends to feel predictable. That’s a quiet advantage. No unexpected steps, no sudden requirements halfway through. Just a clear path from application to approval. It’s not revolutionary, but it works, and that’s often more valuable.

Common unsecured loan types for personal needs

There’s a widespread array of options under the umbrella of Unsecured Finance, and each serves a slightly different purpose. The most common is the unsecured personal loan, often used for consolidating unsecured debt, handling unexpected expenses, or even funding lifestyle upgrades.

Then there are Unsecured Finance options like car loans, which have gained popularity among borrowers who don’t want their vehicle tied to the loan. It sounds minor, but that flexibility matters, especially when plans change or resale becomes a consideration.

A common slip-up is just grabbing the first loan you see. People often go for a general-purpose loan when a more specific option might actually have much better terms. You might not notice the mismatch, but it may cost you more than it should over time.

Business use cases for unsecured finance solutions

For a business, Unsecured Finance is more about the clock than just convenience. Whether it’s a gap in cash flow or a snap opportunity to buy stock, those moments don’t wait around for a traditional bank to spend weeks thinking about an approval.

Many small businesses rely on Unsecured Finance options to stay agile. Not because it’s cheaper, but because it’s faster. That trade-off is usually intentional. Speed allows them to act, and in business, action often carries more weight than marginal savings.

However, there’s a recurring issue. Some businesses begin to rely too heavily on unsecured borrowing without addressing underlying cash flow inefficiencies. Over time, that creates a cycle that becomes harder to manage. Used strategically, it’s powerful. Used casually, it can become expensive.

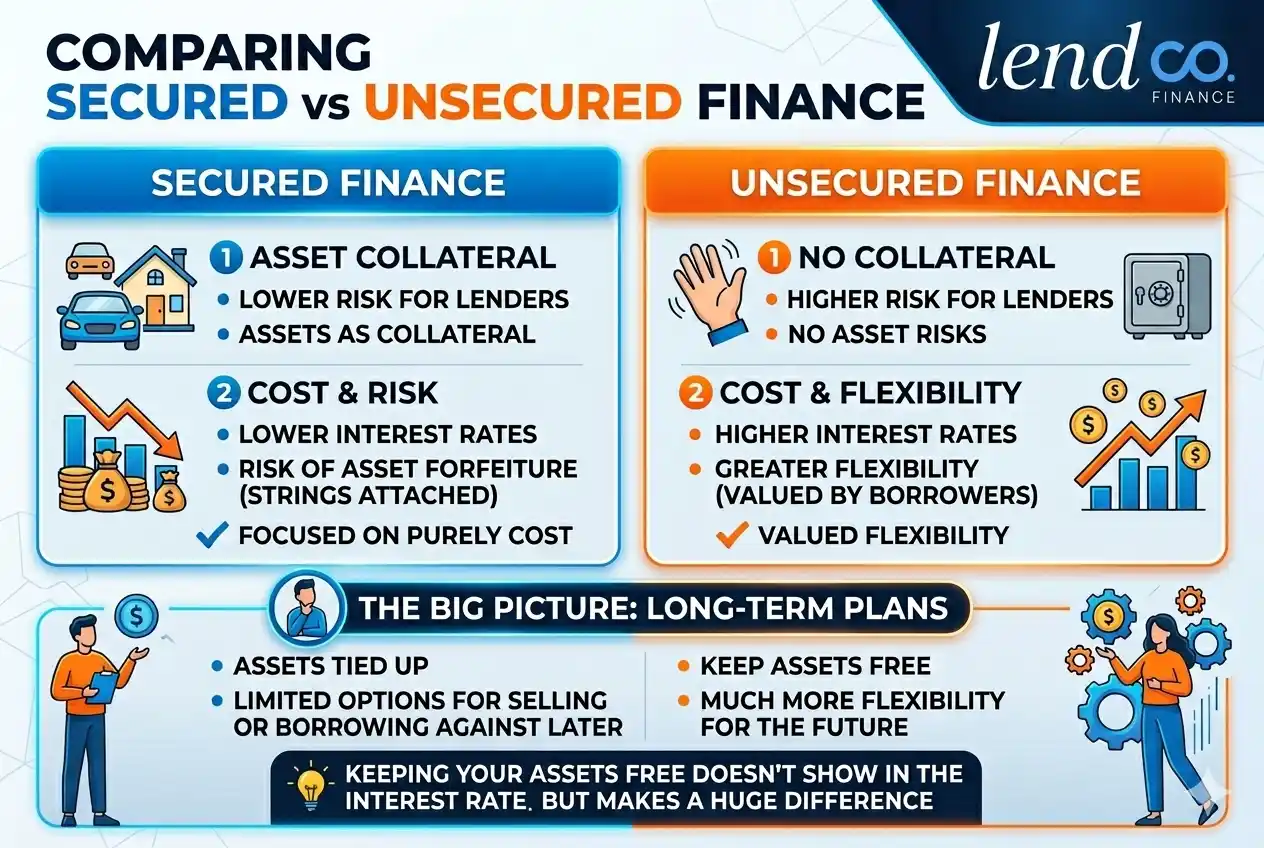

Secured vs Unsecured Finance

| Factor | Secured Loans | Unsecured Finance |

| Collateral | Required | Not required |

| Approval Speed | Slow | Fast |

| Risk to Borrower | High | Lower |

| Interest Rates | Lower | Slightly higher |

| Flexibility | Limited | High |

Costs, risks, and realities borrowers often ignore

There’s no way around it. Unsecured Finance usually comes with higher interest rates. That’s the cost of not providing collateral. Lenders price in the risk, and borrowers absorb it over time.

One thing people often overlook is how those tiny differences in interest rates actually compound. A slightly higher percentage might not feel like much on your monthly bill, but over a few years, it really adds up.

There’s a psychological side to this, too. Because there’s no asset tied to the loan, it’s easy to get a bit casual about the repayments. That’s a dangerous mindset to slip into, as a few missed payments will wreck your credit score pretty quickly. That flexibility actually requires a bit more discipline than people like to admit.

Comparing secured loans and unsecured finance options

The comparison between secured and unsecured lending isn’t new, but it’s often oversimplified. Secured loans are cheaper, yes, but they come with strings attached. Assets are tied up, and that introduces a different kind of risk.

Unsecured Finance, on the other hand, removes that asset risk but increases financial cost. It’s not better or worse; it’s situational. Borrowers who value flexibility tend to lean toward unsecured, while those focused purely on cost often choose secured options.

One thing people often miss is the value of keeping your assets free. If your car or house isn’t tied up in a loan, you have much more flexibility later if you want to sell or borrow against it for something else. You won’t see that benefit in the interest rate, but it makes a huge difference for your long-term plans.

Mistakes people make with unsecured personal loans

Mistakes people make with unsecured personal loans

One of the most common mistakes with an unsecured personal loan is borrowing more than necessary. It sounds obvious, but it happens frequently. Easy access creates a tendency to stretch limits, especially when approvals come quickly.

Repayment structures can also be a bit of a trap if you don’t look closely. Fixed payments feel safe, but they can get tight if your income isn’t steady every month. People often realize this a bit late, especially if they’re trying to manage a few different bits of Unsecured Finance debt at once.

There’s a bit of a psychological trap here, too. It’s easy to treat a loan as a quick, temporary fix rather than a structured financial tool. If you fall into that mindset, it can lead to a cycle of repeated borrowing that actually adds to your financial pressure instead of taking it away.

Smart Tips Before Applying for Unsecured Loans

A few thoughtful steps can make a big difference.

- Check your credit score beforehand

- Compare multiple lenders

- Understand repayment terms

- Avoid borrowing more than needed

A calm, informed approach always wins.

Future trends shaping unsecured finance in Australia

The way Unsecured Finance works in Australia is changing fast. Lenders are moving away from old-school financial snapshots and using real-time data instead. It makes for much more accurate approvals and much faster decisions.

This shift allows for more accurate approvals, but it also changes borrower expectations. Faster decisions become the norm, not the exception. Lendco Finance and similar providers are already operating in this space, where speed and accuracy coexist.

Lending rules are always changing, and right now there’s a massive focus on “responsible lending.” The goal is to make sure people aren’t overextending themselves. Finding that sweet spot between making money accessible and keeping people protected is really going to define the next era of Unsecured Finance in Australia.

Conclusion

In a world that moves this fast, you need options that can keep up. Unsecured Finance is basically a modern way to borrow without the old-school bank delays. Whether you’re covering an emergency or funding a big move, it’s a transparent way to get the funds you need when you actually need them.

Lendco Finance simplifies borrowing with streamlined approvals and clear terms tailored to modern needs. From unsecured personal loans to car finance, everything is designed for ease and speed. Ready to take the next step? Talk to a broker and discover a smarter way to borrow.

Frequently Asked Questions

What is Unsecured Finance in Australia?

To put it in plain English, Unsecured Finance is just a loan where you don’t have to hand over the keys to your house or car as collateral. It’s based entirely on your income and your track record with credit.

How fast can unsecured loans be approved?

A lot of lenders, Lendco Finance included, can now give you an answer in just a few hours. Because the systems are all digital now, the assessment happens way faster than it would at a traditional bank branch, which is a lifesaver when things are urgent.

Are unsecured personal loans safe?

Definitely, unsecured personal loans are a safe and solid option as long as you’re dealing with a reputable lender. You just need to be diligent about checking the fine print for hidden fees. If you’ve got a clear plan to pay it back, it’s a really handy way to get things moving.

Can unsecured finance be used for business purposes?

Absolutely. Many Australian businesses rely on unsecured loans for cash flow, expansion, or operational costs. Since no assets are required, it reduces risk while maintaining access to quick funding.

What’s the difference between unsecured car loans and secured ones?

With unsecured car loans, the big plus is that the car isn’t tied to the debt, giving you a lot more freedom. A secured loan might save you a little bit on the interest rate, but if life throws you a curveball, the lender can actually repossess the car. It’s a trade-off that’s definitely worth weighing up.

Does unsecured debt affect credit scores?

Yes, unsecured debt can impact credit scores depending on repayment behaviour. Timely payments improve credit ratings, while missed payments may lower scores, affecting future borrowing options.